What I Have:

Checking: $1,265.92

Savings: $1,804.19

What I Owe:

Wells Fargo: $82,888.05

Credit Card: $66.69

Target Card: $48.19

Utility: $169.07 (fucking Texas heat)

Med Bill: $22.07

My Plan:

-Pay off Target Card Balance

-Pay of Credit Card (however, I believe my renter's insurance bill goes through tomorrow so the balance will just be upped to $125 again but at least I'll be making a nice chunk payment.

-Pay of Med Bill

-Pay $600 on my student loan

-Save $100-$200 dollars for my fall trip (my goal is to save about $1000)

Sunday, July 14, 2013

Sunday, July 7, 2013

Things I am Willing to Spend Money On // Bucket List

Saving money/getting out of debt isn't solely about being frugal and never having fun (although it can feel that way....a lot). For me, saving money is about eliminating unnecessary spending so I can save towards doing something I really, really, REALLY want to do. I want to make a list where I can keep track of things I want to motivate myself. Skipping a fancy $5 coffee is easy when you think of all the fun stuff that 5 bucks can go towards.

Things I am Willing to Spend Money On

1. Laser hair removal for my lower legs: I found a deal for $500!!

2. New iPhone: around $300

3. Fix my computer: DC jack repair is usually $100

4. Getting my passport: Total cost for fees and paperwork about $165

5. Laser eye surgery: my insurance should pay for some of it and I've seen deals for as cheap as $600 per eye

Bucket List

1. Travel to Canada: Boyfriend has found flights for as cheap as $350. First I have to get my passport (see #4 above)

2. Travel to Europe

3. Travel to East Coast w/ my boyfriend: we're in the middle of planning this trip, I want to save around $1000 to cover all the museums and restaurants I want to visit.

4. Pay off my college debt

5. Own a home

6. Have/adopt/foster a couple of kids

Things I am Willing to Spend Money On

1. Laser hair removal for my lower legs: I found a deal for $500!!

2. New iPhone: around $300

3. Fix my computer: DC jack repair is usually $100

4. Getting my passport: Total cost for fees and paperwork about $165

5. Laser eye surgery: my insurance should pay for some of it and I've seen deals for as cheap as $600 per eye

Bucket List

1. Travel to Canada: Boyfriend has found flights for as cheap as $350. First I have to get my passport (see #4 above)

2. Travel to Europe

3. Travel to East Coast w/ my boyfriend: we're in the middle of planning this trip, I want to save around $1000 to cover all the museums and restaurants I want to visit.

4. Pay off my college debt

5. Own a home

6. Have/adopt/foster a couple of kids

Tuesday, July 2, 2013

After Pay Day

Things have been so hectic. I'm still in the middle of trying to refinance my student loan and it's extremely frustrating. Wells Fargo keeps saying the my Mom doesn't qualify for a cosigner (even though she's my current cosigner). At first we thought that Wells Fargo looking at her debt to income ratio and not considering that most of her debt comes from this particular student loan. Then, in one of my many, many delightful chats with a rep they said that Wells Fargo makes sure not to consider the loan they are currently holding against someone if all they are trying to do is refinance. My mom had already faxed in a few credit reports showing that the only outstanding debt she has is this loan. Of course I tried to explain that to them and they did their usual, "well I can't discuss this with you because you're not the cosigner" bullshit so I had to get off the phone, ring up my mom, and have her call back.

So, she calls back and gets another rep who tries to tell her all sorts of nonsense but luckily I told me mom to request a supervisory review because they were clearly being misleading. We should know if the next few days what they decide. The thing that's REALLY frustrating about all of this??? It's probably all worth nothing. All I want is a low, fixed rate. When I first started paying back this piece of shit loan I wanted a fixed rate because over the long run it's the smarter choice (and Lord knows I'm a stickler for consistency) but all they could offer me at the type was a variable rate of 8.5% versus a fixed rate of 13%. That's so freakin' ridiculous. That's credit card rate ridiculous. This time around I do qualify for a fixed rate as low as 7.49% and I would love that! All I want is to be able to plan down to the penny where my money is going, to not live in fear of this slimy, fat cat banking hiking up my rates on whatever whim they like.

What I have:

Checking: $51.12 (after rent + student loan + lots of ice cream this weekend)

Savings: $1800.41

What I Owe:

Wells Fargo Student Loan: $82,888.05

Credit Card: $58.76

During my lovely chat with Wells Fargo I also decide to cancel my auto withdraw. I'm so sick of being broke every first of the month. I end up with like 20 bucks left over so I have to rely on my credit card or dip into my savings and I hate doing that. Since I'm so ahead in payments I have some wiggle room to figure out a way to pay back a lot but not in such a way that leaves me scrambling.

Sunday, June 30, 2013

Private Student Loans

I've had terrible luck with Wells Fargo (they are the worst, the absolute worst) but I'm in the middle of an application process that could potentially lower my rates. Of course, the entire time Wells Fargo has dragged their heels and are trying to use my current debt (i.e. the student loan they have) against me so I can't get a better interest ray (fuckin' cunts).

BUT I'm sending out energy and prayers that maybe, just maybe the universe and God will smile down upon me and help me get something amazing like a 7% (or lower!) fixed interest rate. If you're in any way spiritual or religious send a prayer out for me?

Thursday, June 27, 2013

6 Month of Loan Payments

I have put off the entry forever. Which is strange because I'm very proud of what I have accomplished. I think I'm just being utterly lazy.

Let's review! I had originally wanted to save 1k a month until I could make a chunk $10,000 payment. However after some research I realized I would get slightly better results by making two monthly payments. So it began, I have lived off of only a few hundred (if not less each month). I pay rent, student loans, bills, gas and grocery and whatever left is mine for either saving or fun. Most months I end up with around $20 bucks in my account before payday.

What I Paid in 2012

Amt Toward Amt Towards

Principle Interest

January $6.54 $739.06

February $116.89 $628.71

March $96.05 $649.55

April $75.11 $670.49

May $118.89 $626.71

June $95.05 $650.55

July $117.29 $628.31

August $97.19 $648.41

September $97.89 $647.71

October $119.47 $626.13

November $99.46 $646.14

December $120.99 $624.61

TOTAL $1,160.82 $7,786.38

Seriously, look at January, only $6 bucks towards principle!!?!?!? Fuck you Wells Fargo. I didn't really keep track of my payments during the first year, I set up automatic payments and just didn't deal with it. I didn't want to think of what was going to principle or how much I was paying in interest or even how long it was going to take. I didn't feel like I had the power to, even if I knew what kind of financial trouble I was in there was nothing I could do about it. Once I got a new (and much, much, much better) job I was able to have the extra cash to take care of business.

What I Paid in 2013 (so far!!)

Amt Toward Amt Toward

Principle Interest

January $101.04 $644.56

January pt2 $708.44 $291.56

February $394.37 $351.23

February pt2 $712.04 $287.96

March $459.96 $285.64

March pt2 $715.86 $284.14

April $403.41 $342.19

April pt2 $719.51 $280.49

May $427.72 $626.71

May pt2 $723.25 $276.75

June $412.41 $333.19

June pt2 $446.45 $253.55

TOTAL $6,224.46 $3,949.14

Payment Amt Toward Amt Toward

MAde Principle Interest

July $745.60 $415.81 $329.79

July pt2 $600.00 $ $

August $ $ $

August pt2 $ $ $

September $ $ $

September pt2 $ $ $

October $ $ $

October pt2 $ $ $

November $ $ $

November pt2 $ $ $

December $ $ $

December pt2 $ $ $

TOTAL $1345.60 $414.81 $329.79

I am so proud of what I've been able to do with this loan. I've paid close to 600% more in just 6 months than what I paid in my first year. I will end up paying close to the same amount of interest (if not slightly lower) this year even though I'm paying so much more. I sometime's get so discouraged because I have so far to go but I just have to remind myself that I'm only 27 years old and I've only been at this for 6 months.

Let's review! I had originally wanted to save 1k a month until I could make a chunk $10,000 payment. However after some research I realized I would get slightly better results by making two monthly payments. So it began, I have lived off of only a few hundred (if not less each month). I pay rent, student loans, bills, gas and grocery and whatever left is mine for either saving or fun. Most months I end up with around $20 bucks in my account before payday.

What I Paid in 2012

Amt Toward Amt Towards

Principle Interest

January $6.54 $739.06

February $116.89 $628.71

March $96.05 $649.55

April $75.11 $670.49

May $118.89 $626.71

June $95.05 $650.55

July $117.29 $628.31

August $97.19 $648.41

September $97.89 $647.71

October $119.47 $626.13

November $99.46 $646.14

December $120.99 $624.61

TOTAL $1,160.82 $7,786.38

Seriously, look at January, only $6 bucks towards principle!!?!?!? Fuck you Wells Fargo. I didn't really keep track of my payments during the first year, I set up automatic payments and just didn't deal with it. I didn't want to think of what was going to principle or how much I was paying in interest or even how long it was going to take. I didn't feel like I had the power to, even if I knew what kind of financial trouble I was in there was nothing I could do about it. Once I got a new (and much, much, much better) job I was able to have the extra cash to take care of business.

What I Paid in 2013 (so far!!)

Amt Toward Amt Toward

Principle Interest

January $101.04 $644.56

January pt2 $708.44 $291.56

February $394.37 $351.23

February pt2 $712.04 $287.96

March $459.96 $285.64

March pt2 $715.86 $284.14

April $403.41 $342.19

April pt2 $719.51 $280.49

May $427.72 $626.71

May pt2 $723.25 $276.75

June $412.41 $333.19

June pt2 $446.45 $253.55

TOTAL $6,224.46 $3,949.14

Payment Amt Toward Amt Toward

MAde Principle Interest

July $745.60 $415.81 $329.79

July pt2 $600.00 $ $

August $ $ $

August pt2 $ $ $

September $ $ $

September pt2 $ $ $

October $ $ $

October pt2 $ $ $

November $ $ $

November pt2 $ $ $

December $ $ $

December pt2 $ $ $

TOTAL $1345.60 $414.81 $329.79

I am so proud of what I've been able to do with this loan. I've paid close to 600% more in just 6 months than what I paid in my first year. I will end up paying close to the same amount of interest (if not slightly lower) this year even though I'm paying so much more. I sometime's get so discouraged because I have so far to go but I just have to remind myself that I'm only 27 years old and I've only been at this for 6 months.

Friday, June 21, 2013

Some much needed motivation....

It's not easy being 27 (fast approaching 28) living in a rented house with a boyfriend. Even the most empowered feminist can feel down when you don't get to experience the big "life things" that most people do. Articles like this make me realize that the people that I admire the most definitely had a delayed life start because they worked for years on their dreams. Such positive motivation to keep my chin up :)

Monday, June 17, 2013

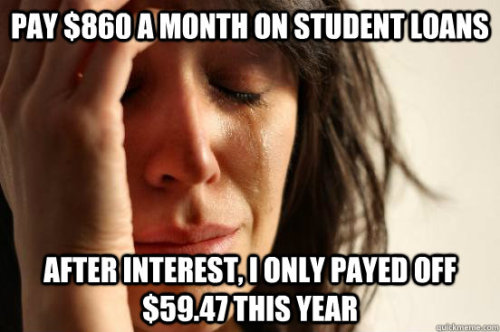

After Bill Pay

|

| Found this while online, isn't it terrifying? This is why I'm so aggressive when it comes to wiping out my debt. |

What I have:

Checking: $225.05

Savings: $1800.64

What I owe:

Credit Card: $17.31**

Student Loan: 83,303.86

Like I said in a previous post instead of my usual $1000 chunk payment I went a little soft this time so I could catch up on bills. I'm still really excited because my next payment should knock me down to 82k which is so freaking exciting. I can't believe how much that I have paid off in just 6 months. I still get a little bummed when I think about how far I have to go and how many roadblocks that I might face but I just have to keep staying positive. The one thing that I do know is that I have more student debt than most people and that with all my hard work I will pay off my debt faster than most people even dream about <3

**I seriously paid off my entire credit card and then the auto payment went through for my gym membership.

Friday, June 14, 2013

Pay Day Check In

I love pay day :) However this pay day is going to be slightly different than previous pay days. I really have to catch up on bills. As awesome as it feels to pay off so much from my student loans it is terrible to realize you only have $50 bucks to live off of for two weeks and some how try to stretch groceries and gas out of that.

What I have:

Checking: $1289.22

Savings: $1800.63

What I owe:

Utilities: $150

Credit Card: $185.86

Student Loan: $83,750.31

My Plan:

-Pay off Credit Card

-Pay Utility Bill

-Pay $700 to student loan

Once the dust clears from that I'm planning on going grocery shopping and purchasing my father a Father's Day gift. After all that's done I should have around $100-$50 remaining. I want to put some additional funds in my savings. I really prefer at least $2,000 in savings and I want to eventually grow it. I think I need to work into my budget a monthly savings contribution.

What I have:

Checking: $1289.22

Savings: $1800.63

What I owe:

Utilities: $150

Credit Card: $185.86

Student Loan: $83,750.31

My Plan:

-Pay off Credit Card

-Pay Utility Bill

-Pay $700 to student loan

Once the dust clears from that I'm planning on going grocery shopping and purchasing my father a Father's Day gift. After all that's done I should have around $100-$50 remaining. I want to put some additional funds in my savings. I really prefer at least $2,000 in savings and I want to eventually grow it. I think I need to work into my budget a monthly savings contribution.

Tuesday, June 4, 2013

After Bill Pay

Ugh, right now my finances suck. Not really terrible pleased with where I'm at currently.

What I have

Checking: $17.68

Savings: $1823.94

What I Owe

Student Loan: $83.750.71

Credit Card: $165.86

I realized something the other day. My spending freeze is like an extreme diet. Instead of going slow and steady, hitting the gym and watching my intake I'm starving myself and running marathons. I'm really proud of how much I've paid off on my student loans but right now I need to work out a livable budget.

I've tried to balance too much on too little. My budget is perfect when things are going right but when they're not or when something comes up (car issues, birthdays, computer problems) it leaves me scrambling and without any money (example: I have $17 bucks to live off of for the next two weeks).

When I get paid again on the 15th instead of immediately paying a huge chunk payment and living off the rest, I'm going to pay off my credit card and pay any remaining bills (I think my utilities should be due around that time) with the remaining I'll then get food and maybe a tank of gas AND THEN I'll pay a chunk towards my student loan. I'm bummed because I won't see the huge decrease I like but I'm getting so tired of being so stressed and broke. I realized the other day that I'm not really broke at all, I make awesome money and I'm causing myself financial hardship by living outside of my means with my student loan repayments. Living within your means doesn't just refer to spending habits but saving habits and debt repayment habits.

In happier news: Can you believe how freakin' close I am to paying off 10k in principal on this loan?!?!?!?! Realistically I consider myself only in repayment for this year (I think the first year I only knocked off something sad like $900 in principal). In 6 months I have paid off $6,250 in principal!!!!

Monday, June 3, 2013

Resolution Check In: Halfway through 2013

I can't believe that this year is almost over with. Time is seriously zooming past. Since this year is halfway over I wanted to check in on my New Years Resolutions to see if I'm making any progress or if I need to re-evaluate my goals.

New Years Resolutions:

1. Run Capital 10k in one hour or less: Sort of? I ran the Capital 10k in 1 hour and 4 minutes which is (obviously) 4 minutes longer than 1 hour but it is 10 minutes less than the first time I ran the Cap10k. I still want to improve on my speed for running but I'm happy with my performance in the race.

2. Complete Fun Run: I ran the Color Run a few weeks ago and it was a blast. I honestly think it was some of my best running time too. One of the people in my race group had an awesome pace and I kept up the entire way. I definitely think I broke my usual 10 minute mile.

4. No desserts for the month of January: I did really well at this goal. I was surprised too because I'm such a sugar addict (for example, during this 2 day weekend I got ice cream 3 times). I've definitely had a few bad days in my diet recently but for the most part I'm happy with where I'm at health wise.

5. 50 squats a day during the month of January: Loved and hated this challenge. This plus weight lifting completely changed my legs. I'm a classic pear and I thought it was impossible to lose weight from my thighs but weight training has made them more toned and sexier. I think it's incredible funny/ironic that itty bitty 90 lbs girls long for a thigh gap and I have one now simple due to how wide set my thighs are.

6. Save at least $1000 a month for Student loans and make a $10,000 chunk payment: This was my original goal until I crunched the numbers and realized I would see better results with more payments. I plan on making a post about my success over the last 6 months in repayment. I'm already down around $7000 :)

7. Get a new driver's license: Never doubt the power of allowing yourself to accomplish easy goals. Feeling accomplished and driven is so good for the psyche.

8. Go to the gyno and try to find a birth control I like: Going to the doctors this week, not sure about birth control. Obviously, I don't want a baby right now because they're expensive and I have no money but I have never found a BC pill that I like. I figure I'll discuss with my doctor my options and see if I can find one that works for me.

10. Sign up for the Capital 10k: Obviously couldn't complete Goal #1 without this but seriously, allowing yourself to accomplish easy goals or tasks is so motivating.

11. Redecorate my bedroom: Found an amazing deal for an entire new bed set for only like $200 bucks. God new curtains and new bedspread and the room looks so much more grown up now.

12. Write a short story of book: My computer crapped out months ago and I just don't feel comfortable writing on my boyfriends computer. I'm hoping to get my computer fixed soon and I definitely want to start writing again.

13. Reupholster my ugly painted chair: I honestly don't know if I'm ever going to do this. The chair is gorgeous to look at (very rustic and shabby chic) but soooo gross to sit on (crunchy fabric paint).

14. Learn more hairstyles than the same bullshit I constantly wear: Nope :( However this is the healthiest my hair has been in 10 years. I haven't dyed my hair in over a year (maybe longer) and I've cut off all the processed stuff. My hair is much lighter in color than I had anticipated but I look pretty good. Sometime it's hard to fight the urge to dye it all of the time but I just remember how annoying upkeep is and how expensive constantly dying it can be.

15. Cook new recipes: Yes? No? I've definitely tried new things but not on such a level that I feel it justifies crossing this item off. I had a completely lazy weekend where I spent hours on Pinterest so I have lots of new recipes to try.

Sunday, June 2, 2013

Friday, May 31, 2013

Pay Day Check In

Today is pay day so I'm checking in with all of my finances and bills.

What I Have:

Checking Account: $1,313.28

Savings: $1,823.94

Wallet: nada

What I Owe:

Student Loan: $84,162.72

Credit Card: 248.55

Where my money is going:

I'm paying my typical 1st of the month loan payment of $745.60 and rent is $400, that leaves me with $167.68. I'm going to make a $100 payment on my credit card. I might pay off the rest of the card from money in my savings.

Why is my card so high? OKAY. So I know I'm on a vague-ish spending freeze. However, there are some things in life that I really, really, reallllllly want to do. Bucket list things (I plan on making a post about them later!). One of them is laser hair removal. I know that sounds lame since most people's bucket list items are like, climb a mount, see Spain, blah blah blah. Well good for you but I don't want to ever shave my armpits again. A bunch of people I work with have had it done and I felt the results and they are so freakin' amazing. I'm not sure what I was expecting but I was totally blown away by the quality of the work. Anyway, I had pretty much made up my mind that I wanted it done and then just yesterday I get an Amazon Local deal saying I could get 6 treatments on a small area for only $99. That is absurd. Most places charge any where from $600-$1000 for small areas. I checked online and the places reviews are good and I called and asked a bunch of questions. As I was talking to the lady I ended up just purchasing the package.

Yes, I should spend $99 towards bills or food or gas or whatever but I have ZERO regrets about doing something awesome for myself. Especially because of how much money I'm saving. I go in for my first appointment tomorrow. I've already decided that once this area is all done I'm going to do my legs (at least the lower half) sometime next year. Because I'm broke/cheap I'll wait until there's a great deal but when that deal comes up I won't feel any guilt about getting it :)

What I Have:

Checking Account: $1,313.28

Savings: $1,823.94

Wallet: nada

What I Owe:

Student Loan: $84,162.72

Credit Card: 248.55

Where my money is going:

I'm paying my typical 1st of the month loan payment of $745.60 and rent is $400, that leaves me with $167.68. I'm going to make a $100 payment on my credit card. I might pay off the rest of the card from money in my savings.

Why is my card so high? OKAY. So I know I'm on a vague-ish spending freeze. However, there are some things in life that I really, really, reallllllly want to do. Bucket list things (I plan on making a post about them later!). One of them is laser hair removal. I know that sounds lame since most people's bucket list items are like, climb a mount, see Spain, blah blah blah. Well good for you but I don't want to ever shave my armpits again. A bunch of people I work with have had it done and I felt the results and they are so freakin' amazing. I'm not sure what I was expecting but I was totally blown away by the quality of the work. Anyway, I had pretty much made up my mind that I wanted it done and then just yesterday I get an Amazon Local deal saying I could get 6 treatments on a small area for only $99. That is absurd. Most places charge any where from $600-$1000 for small areas. I checked online and the places reviews are good and I called and asked a bunch of questions. As I was talking to the lady I ended up just purchasing the package.

Yes, I should spend $99 towards bills or food or gas or whatever but I have ZERO regrets about doing something awesome for myself. Especially because of how much money I'm saving. I go in for my first appointment tomorrow. I've already decided that once this area is all done I'm going to do my legs (at least the lower half) sometime next year. Because I'm broke/cheap I'll wait until there's a great deal but when that deal comes up I won't feel any guilt about getting it :)

Wednesday, May 29, 2013

This about sums it up

I have no problem paying off my student loans but let's take a real long look at what my generation has had to pay in tuition fees and interest rates. This shit is ridiculous.

Tuesday, May 28, 2013

You Might Be Broke If......

-You've ever re-used a coffee filter

-You have no shame in using rubber bands and tape to hold together everyday items

-You can easily ignore any sound that might mean an appliance is breaking

-You have paid for groceries in loose change

-You experience overwhelming joy when there's free food at work

Sunday, May 19, 2013

Financial Update: After Bill Pay

So I did a Pay Day check in a few days ago but I wanted to re-check in (checker in? No, that's not right...) to see my finances after I spent a late Mother's Day with my Mom and after most of my bill payments went through.

Checking: $152.42

Savings: $1822.20

Pocket Book: Like $2 bucks?? I spent the remainder of my cash on Powerball tickets (that did not go well).

What I owe on my credit card: $119.92

What I owe Wells Fargo: $84,162.72

I treated my mom to lunch which cost $50 (put on my credit card) BUT she treated me to a full tank of gas, a hair cut, and a mani/pedi. I might go ahead and pay another $50 or so on my credit card but probably closer to next pay day. I still need to go grocery shopping but that should only cost me around $50.

I can't believe how far down my loan has gone in only 5 months. I'm so close to paying off $10,000 in principle. I think once that happens (and I potentially get a raise sometime in October) I might start shifting around how much I pay. I want to help my mom with the student loan that she has for me. She owes around $38k and I'd like to help her pay it off so she can save for retirement.

I keep looking at the financial road map I made; in just two years I will be close to only owing around $50,000. Then I can slow down on the payments and start saving for a house. I try to broach the idea of buying a house with my boyfriend but he doesn't really seem that into it which is a bummer but not terribly unexpected. Like most things in life I'll probably do that on my own (or with the help of my mom, haha). I figure I can easily save up the $20,000 or so down payment and I should have rocking credit so hopefully I can find a cute little house to call my own.

Checking: $152.42

Savings: $1822.20

Pocket Book: Like $2 bucks?? I spent the remainder of my cash on Powerball tickets (that did not go well).

What I owe on my credit card: $119.92

What I owe Wells Fargo: $84,162.72

I treated my mom to lunch which cost $50 (put on my credit card) BUT she treated me to a full tank of gas, a hair cut, and a mani/pedi. I might go ahead and pay another $50 or so on my credit card but probably closer to next pay day. I still need to go grocery shopping but that should only cost me around $50.

I can't believe how far down my loan has gone in only 5 months. I'm so close to paying off $10,000 in principle. I think once that happens (and I potentially get a raise sometime in October) I might start shifting around how much I pay. I want to help my mom with the student loan that she has for me. She owes around $38k and I'd like to help her pay it off so she can save for retirement.

I keep looking at the financial road map I made; in just two years I will be close to only owing around $50,000. Then I can slow down on the payments and start saving for a house. I try to broach the idea of buying a house with my boyfriend but he doesn't really seem that into it which is a bummer but not terribly unexpected. Like most things in life I'll probably do that on my own (or with the help of my mom, haha). I figure I can easily save up the $20,000 or so down payment and I should have rocking credit so hopefully I can find a cute little house to call my own.

Wednesday, May 15, 2013

Pay Day Finances

I want to start monitoring my spending/debt more closely. I feel that it will help to keep me more strict and honest with my budget plus it really feeds my Type A personality to organize everything.

Today I got paid (yay!) which means that I have to go in and pay all my bills (boo!). Here's the current breakdown:

What I have:

Checking: $1318.93

Savings: $1825.18

Pocket book: $20 from babysitting

What I owe:

Credit card: $109.36

Utilities: $116.51

I plan on using the money I have from babysitting to put gas into my tank (I'm going home this weekend for a late mother's day and will definitely need it). I'm also babysitting tonight and the $30 or $40 bucks I earn from that will go towards paying for photos I had printed for my Mom's Mother's Day gift (only $10!) and then a birthday happy hour I plan on attending this Friday. If I pay all of my bills plus my usual $1000 on my student loans I will only have $93 left in my checking and I will have put nothing away for savings. Sort of a bummer.

My plan is to pay my utility bill in full (because lights and air conditioning are pretty nifty), pay $50 towards my credit card, and pay $1000 towards my student loan.

I find the only way I can stomach paying so much on my student loan is to do it very early in the morning on pay day. That way I'm still sleepy/out of it and my brain doesn't have time to process all the fun things I could do with an extra grand each month. Plus, since it's pay day I'm not used to seeing so much in my bank account. Most days when I log into my account I see something awesome like I only have $27 bucks to live on for 2 weeks.

The thing that makes it easier is that I'm telling myself that I'm just doing it for one year. Now I do have a 5 year plan to pay off my 90k student loan but all I'm holding myself accountable for is one year. I just have to pay a lot this year and next year things will be easier. I will have paid it (hopefully) down into the $70,000 ish area which will be easier to deal with/look at/live with than 90K. Once I've done my first year I'll look at my budget and realize that by the end of year two I should have it down to around $50k. Once I get it below $50k I can slow down a bit. The interest each month will be lower, it's a more typical student loan amount than close to $100k. I'll be able to save more for a house and maybe even feel more comfortable spending money on fun things. I've just got to take it one pay day at a time.

Today I got paid (yay!) which means that I have to go in and pay all my bills (boo!). Here's the current breakdown:

What I have:

Checking: $1318.93

Savings: $1825.18

Pocket book: $20 from babysitting

What I owe:

Credit card: $109.36

Utilities: $116.51

I plan on using the money I have from babysitting to put gas into my tank (I'm going home this weekend for a late mother's day and will definitely need it). I'm also babysitting tonight and the $30 or $40 bucks I earn from that will go towards paying for photos I had printed for my Mom's Mother's Day gift (only $10!) and then a birthday happy hour I plan on attending this Friday. If I pay all of my bills plus my usual $1000 on my student loans I will only have $93 left in my checking and I will have put nothing away for savings. Sort of a bummer.

My plan is to pay my utility bill in full (because lights and air conditioning are pretty nifty), pay $50 towards my credit card, and pay $1000 towards my student loan.

I find the only way I can stomach paying so much on my student loan is to do it very early in the morning on pay day. That way I'm still sleepy/out of it and my brain doesn't have time to process all the fun things I could do with an extra grand each month. Plus, since it's pay day I'm not used to seeing so much in my bank account. Most days when I log into my account I see something awesome like I only have $27 bucks to live on for 2 weeks.

The thing that makes it easier is that I'm telling myself that I'm just doing it for one year. Now I do have a 5 year plan to pay off my 90k student loan but all I'm holding myself accountable for is one year. I just have to pay a lot this year and next year things will be easier. I will have paid it (hopefully) down into the $70,000 ish area which will be easier to deal with/look at/live with than 90K. Once I've done my first year I'll look at my budget and realize that by the end of year two I should have it down to around $50k. Once I get it below $50k I can slow down a bit. The interest each month will be lower, it's a more typical student loan amount than close to $100k. I'll be able to save more for a house and maybe even feel more comfortable spending money on fun things. I've just got to take it one pay day at a time.

Sunday, May 5, 2013

Birthday on the Cheap!

I just spent an amazing birthday weekend with my sister and I'm pretty proud of how I kept my spending under control.

Here's the wrap-up

Food:

I mentioned in my last post about how cheap and easy home made birthday cake and ice cream is. But, most people don't like to live off of just cake and sweets so we had to pick up some food and drinks. If you've read this blog at all you know I fancy booze and my absolute favorite liquor store is Cost Co. You don't have to be a member to purchase liquor (at least at the one's in Texas, they have a separate room for the hard liquor and any one can buy from it). My sister and I picked up a giant bottle of Tequila for only $20 bucks and then went to HEB and got some regular house food (morning and lunch staples like bagels, bananas, eggs, and yogurt) as well as ingredients for quesadillas. My total bill was only $44 bucks which isn't the best but not too bad for food for a week.

Entertainment

My sister loves coming up to Austin and shopping at stores they don't have in her town. We entertained ourselves for hours on window shopping. We're also both pop culture shows so we watched a ton of TV and movies. She had purchased the tickets for the show earlier so that was a cost I didn't have to worry about.

Unnecessary but lovely purchase:

Bought my boyfriend lunch at a great gourmet burger joint (my sister insisted on paying for herself): $28 bucks

A new pair of Betsey Johnson sunglasses: $20 bucks

A new wall plug and 3 new scents from Bath and Body Works:$20

Yes, it was unnecessary and not really apart of my budget to spend $68 dollars on these things. BUT I manage to live off of around $300 a month (covering my utility bill, gas, food, and social life) because I spend every other dime on student loans. I haven't purchased new sunglasses in more than 5 years. The one's I have been using were a pair of Betsey Johnson's my ex bought for me years ago.

Here are my new glasses:

Here's the wrap-up

Food:

I mentioned in my last post about how cheap and easy home made birthday cake and ice cream is. But, most people don't like to live off of just cake and sweets so we had to pick up some food and drinks. If you've read this blog at all you know I fancy booze and my absolute favorite liquor store is Cost Co. You don't have to be a member to purchase liquor (at least at the one's in Texas, they have a separate room for the hard liquor and any one can buy from it). My sister and I picked up a giant bottle of Tequila for only $20 bucks and then went to HEB and got some regular house food (morning and lunch staples like bagels, bananas, eggs, and yogurt) as well as ingredients for quesadillas. My total bill was only $44 bucks which isn't the best but not too bad for food for a week.

Entertainment

My sister loves coming up to Austin and shopping at stores they don't have in her town. We entertained ourselves for hours on window shopping. We're also both pop culture shows so we watched a ton of TV and movies. She had purchased the tickets for the show earlier so that was a cost I didn't have to worry about.

Unnecessary but lovely purchase:

Bought my boyfriend lunch at a great gourmet burger joint (my sister insisted on paying for herself): $28 bucks

A new pair of Betsey Johnson sunglasses: $20 bucks

A new wall plug and 3 new scents from Bath and Body Works:$20

Yes, it was unnecessary and not really apart of my budget to spend $68 dollars on these things. BUT I manage to live off of around $300 a month (covering my utility bill, gas, food, and social life) because I spend every other dime on student loans. I haven't purchased new sunglasses in more than 5 years. The one's I have been using were a pair of Betsey Johnson's my ex bought for me years ago.

Here are my new glasses:

They were originally around $70 so paying only $20 for them was a steal. Plus they came with an adorable bright pink sunglass case.

I feel pretty good about this weekend. I have around $70 in my checking account and around $100 on my credit card. I don't have any bills on my credit card due and when I get paid on the 15th I can pay off my credit card and add a little more to my savings.

I've mentioned before how much I really enjoy And Then We Saved. Their big idea is a spending fast. Basically spending on only the absolute necessities (food, housing) and either saving the rest or paying off debt. I realized that even though I sometimes spend some cash on unnecessary things I'm pretty much on spending fast. 70% of my income goes towards student loans (literally, I did math to figure that out, that's not just a guess). And like I said above the rest is spent on rent, food, gas, and utilities. Yes, anything after that probably could go into savings but I'm glad it goes into fun things like Fun Run races (I did the color run this weekend and it was amazing!) or shoes or sunglasses or unnecessary scent thingies from Bath and Body Works.

Friday, May 3, 2013

My Sister's Bday Weekend

My sister is coming up to celebrate her birthday weekend and I'm excited/nervous to host and entertain under a budget. We're going to go and see a show and then spend the rest of the weekend hanging out and enjoying quality time.

I'm hoping that I can keep track of my spending this week. Here's what's gone down so far:

Birthday Cake:

$1 on chocolate cake mix

$2 on 2 chobani yogurts

=

$3 cake!!!

Ice Cream and Cake Icing:

$1 on small container of whole milk

$3 on large container of heavy cream

=$4 birthday extras!

I have an ice cream machine and I'm a pro at making my own icings from my vegan days so whipping up the cake extras was a breeze. It's pretty incredible to spend $7 bucks for cake and ice cream.

Birthday Gift:

$1 on basket

$12 on two bags of specialty coffee

$2 for 2 cute dollar store mugs

=

$15 Bday present

Pinterest has been a great inspiration for cheap but great basket gifts. My sister loves coffee and presenting coffee plus mugs in a basket makes it seem like such a bigger gift. I really hope she enjoys it.

Once she gets here we're going to stop by the grocery store to pick up food (eating in is much cheaper than dining out constantly). I'm so incredible excited for this weekend :)

I'm hoping that I can keep track of my spending this week. Here's what's gone down so far:

Birthday Cake:

$1 on chocolate cake mix

$2 on 2 chobani yogurts

=

$3 cake!!!

Ice Cream and Cake Icing:

$1 on small container of whole milk

$3 on large container of heavy cream

=$4 birthday extras!

I have an ice cream machine and I'm a pro at making my own icings from my vegan days so whipping up the cake extras was a breeze. It's pretty incredible to spend $7 bucks for cake and ice cream.

Birthday Gift:

$1 on basket

$12 on two bags of specialty coffee

$2 for 2 cute dollar store mugs

=

$15 Bday present

Pinterest has been a great inspiration for cheap but great basket gifts. My sister loves coffee and presenting coffee plus mugs in a basket makes it seem like such a bigger gift. I really hope she enjoys it.

Once she gets here we're going to stop by the grocery store to pick up food (eating in is much cheaper than dining out constantly). I'm so incredible excited for this weekend :)

Tuesday, April 16, 2013

How to Cope with Spending Money

I recently had to drop close to $200 on car repairs. My monthly "take home" pay (after bills) ends up being around that much. It's very hard to live off of $200 a month and it's even harder to have to spend 100% of that on unexpected life hiccups.

I pushed off my car repairs for MONTHS. I really, really, really didn't want to do them. It was big-ish stuff; the usual oil change stuff plus new transmission fluid and coolant. Unfortunately my car started acting so funny and so off that I just had to go in. Luckily, I've been a pretty steady client of Jiffy Lube and I was able to use a 35% off coupon to help.

It's really hard to live on a budget. Paying off debt feels amazing but it also creates a lot of anxiety and guilt. The idea of spending un-budgeted money caused me great stress. The total bill was around $300 but I ended up spending less than $200 because of the coupon. Even though I saved a boat load and got the best deal that I could I still felt stress/sadness/guilt over it.

That's what I want to talk about today. Ways to cope with spending money

1. Recognize that you are not spending money on frivolous things.

I could have easily spent $200 on clothes or shoes or trips. On anything really. It's so sad because sometimes I honestly day dream about that. About taking half of my extra $1000 student loan payment and buying so many new clothes. But I don't. I work really hard and buy just what I need and unfortunately, at this time, my car needed some work.

2. You can't budget life

It pains me to say this but you simple can't plan for life. You can try and come really, really close but life just has too many bumps and turns. So yes, I budget as best I can and 90% of the time I'm right on track but I have to accept and EXPECT that life will throw me a curve ball every once in a while.

3. You will always be able to more later

My budget won't always be this tight. I will get raises and bonuses and unexpected windfalls in the future. So yes, I feel guilty now for spending money but I know that if I ever come into more money I will be responsible with it and budget accordingly. Reminding myself of how responsible I really am helped with the feelings of guilt.

4. Spending a little now prevents big spending in the future

Okay, spending $200 bucks sucks. Badly. BUT, spending $1000 + dollars because I ignored my car would realllllly suck. So I pay a little now and I prevent big catastrophes in the future. No break downs on the side of the roads, no towing fee, or rental car hassle. By keeping the things that I have now nice and in good condition I am preventing future unnecessarily spending.

Now this list isn't as comprehensive as I would like but I felt it was really important to get it down. It makes me feel better. I'm trying really hard to budget well and pay off my debts and set backs hurt. In the 4 months that I have been making extra student loan payments I have paid 400% more than I did my entire first year :) I am doing amazing and I sometimes have to remind myself of that.

I pushed off my car repairs for MONTHS. I really, really, really didn't want to do them. It was big-ish stuff; the usual oil change stuff plus new transmission fluid and coolant. Unfortunately my car started acting so funny and so off that I just had to go in. Luckily, I've been a pretty steady client of Jiffy Lube and I was able to use a 35% off coupon to help.

It's really hard to live on a budget. Paying off debt feels amazing but it also creates a lot of anxiety and guilt. The idea of spending un-budgeted money caused me great stress. The total bill was around $300 but I ended up spending less than $200 because of the coupon. Even though I saved a boat load and got the best deal that I could I still felt stress/sadness/guilt over it.

That's what I want to talk about today. Ways to cope with spending money

1. Recognize that you are not spending money on frivolous things.

I could have easily spent $200 on clothes or shoes or trips. On anything really. It's so sad because sometimes I honestly day dream about that. About taking half of my extra $1000 student loan payment and buying so many new clothes. But I don't. I work really hard and buy just what I need and unfortunately, at this time, my car needed some work.

2. You can't budget life

It pains me to say this but you simple can't plan for life. You can try and come really, really close but life just has too many bumps and turns. So yes, I budget as best I can and 90% of the time I'm right on track but I have to accept and EXPECT that life will throw me a curve ball every once in a while.

3. You will always be able to more later

My budget won't always be this tight. I will get raises and bonuses and unexpected windfalls in the future. So yes, I feel guilty now for spending money but I know that if I ever come into more money I will be responsible with it and budget accordingly. Reminding myself of how responsible I really am helped with the feelings of guilt.

4. Spending a little now prevents big spending in the future

Okay, spending $200 bucks sucks. Badly. BUT, spending $1000 + dollars because I ignored my car would realllllly suck. So I pay a little now and I prevent big catastrophes in the future. No break downs on the side of the roads, no towing fee, or rental car hassle. By keeping the things that I have now nice and in good condition I am preventing future unnecessarily spending.

Now this list isn't as comprehensive as I would like but I felt it was really important to get it down. It makes me feel better. I'm trying really hard to budget well and pay off my debts and set backs hurt. In the 4 months that I have been making extra student loan payments I have paid 400% more than I did my entire first year :) I am doing amazing and I sometimes have to remind myself of that.

Monday, April 8, 2013

Sunday, March 24, 2013

DIY: Pillow Fix

I have a junk back. Always have pretty much. I have slight scoliosis and the twist plus my usual routine of running/weight lifting don't help. I have an awesome back support pillow that I got from target years ago. It wraps around my body and has arm rests and even a cute little pocket for your remote. Over the years it has deflated from overuse and offered less and less support.

Instead of buying a new one I figured out that with a little love I could bring it back to life.

Pillow Before:

Instead of buying a new one I figured out that with a little love I could bring it back to life.

Pillow Before:

Pillow After:

Please excuse the light saturated photo :/

This was the easy DIY // up-do that I have ever done. I've been spring cleaning my house top to bottom and I have 3 assorted pillows that have come to the end of their little pillow lives. I cut a small hole in the bottom of my back support pillow and used the stuffing from my old bed pillow to fluff it up. It took 1 full bed pillow plus an Ikea couch pillow to re-stuff my back pillow but it feels amazing and looks so much better. The only cost of this project was around $2 for a little thread and needle kit.

Thursday, March 14, 2013

Helpful Links

Two posts in one day! Miraculous. I've been having great luck today finding really helpful sites for dealing with student loans and I thought I'd post them up for everyone :)

National Student Loan Data System: Monitors how much you have in student loans so you can accurately start figuring out how to cut it down.

Student Loan Calculator: Just plug in what you owe, how much you plan on paying monthly and at what percentage and it tells you how much time it'll take to pay it off. Awesome.

And Then We Saved: A really sweet blog that features tons of inspiring stories and helpful hints for leaving a debt free life.

National Student Loan Data System: Monitors how much you have in student loans so you can accurately start figuring out how to cut it down.

Student Loan Calculator: Just plug in what you owe, how much you plan on paying monthly and at what percentage and it tells you how much time it'll take to pay it off. Awesome.

And Then We Saved: A really sweet blog that features tons of inspiring stories and helpful hints for leaving a debt free life.

Revisiting my thankful place...

First let's start this post with the required, "I'm terrible at updating this thing...blah blah blah...I swear to post more...blah blah blah".

The past few weeks I hit a bit of a rough spot. Just felt really bummed about my place in life. I'm 27 and I'm no where near these big life events that I think I should be. Luckily, I'm feeling so much better and happier and I realized that it's been far too long since I posted things that I'm thankful for. I spend so much time on this blog complaining about my debt and my bills and I should focus more on the riches I do have.

What I'm Thankful For:

1. Paying off my debt: in the past three months I have paid off THREE times as much of my principle debt than I have in the past year. The first year that I was paying off my college loan I only knocked off about $1200 in principle now I'm knocking off around that much each month. It's been incredible hard to see so much of my check go each month to bills but I know at the end of this year I'll be so much happier and that much closer to ultimately paying my debt off.

2. My friends and family: I have such supportive and amazing family. That really all there is to it. In this wild and crazy world I have so many people that I love that love me back and that's really very special.

3. My boyfriend: Yeah, he gets a number all his own. I seriously love this guy. I never thought I would live with someone again and now I can't imagine living without him. When he's not home I get so sad and when we're together it's the best part of my day. Our work schedules are completed jacked and we sometimes go days with only seeing each other briefly at night but last night we actually went to bed at the same time and it was so nice. Just to lay with him and laugh and fall asleep together.

4. My job: I really do love my job and even on days where it's hard I'm still so luckily to do what I love. I was able to go from a job with low pay and terrible treatment to a job with amazing pay, great hours, and awesome co-workers. I'm really blessed.

There's a million more daily things I'm thankful for: great weather, good running trails, Dr Who on instant Netflix, insane genes that allow me to eat my weight in sugar and not get diabetes, sunshine, laughter, and so much more. Even though it's taking me a few months to save the extra cash I'm finally going to be able to buy a sewing machine and I'm so excited to start sewing again. I want to try my hand at DIY clothes/up cycling and quilting. I'm hoping to be able to post more about cheap DIY projects.

The past few weeks I hit a bit of a rough spot. Just felt really bummed about my place in life. I'm 27 and I'm no where near these big life events that I think I should be. Luckily, I'm feeling so much better and happier and I realized that it's been far too long since I posted things that I'm thankful for. I spend so much time on this blog complaining about my debt and my bills and I should focus more on the riches I do have.

What I'm Thankful For:

1. Paying off my debt: in the past three months I have paid off THREE times as much of my principle debt than I have in the past year. The first year that I was paying off my college loan I only knocked off about $1200 in principle now I'm knocking off around that much each month. It's been incredible hard to see so much of my check go each month to bills but I know at the end of this year I'll be so much happier and that much closer to ultimately paying my debt off.

2. My friends and family: I have such supportive and amazing family. That really all there is to it. In this wild and crazy world I have so many people that I love that love me back and that's really very special.

3. My boyfriend: Yeah, he gets a number all his own. I seriously love this guy. I never thought I would live with someone again and now I can't imagine living without him. When he's not home I get so sad and when we're together it's the best part of my day. Our work schedules are completed jacked and we sometimes go days with only seeing each other briefly at night but last night we actually went to bed at the same time and it was so nice. Just to lay with him and laugh and fall asleep together.

4. My job: I really do love my job and even on days where it's hard I'm still so luckily to do what I love. I was able to go from a job with low pay and terrible treatment to a job with amazing pay, great hours, and awesome co-workers. I'm really blessed.

There's a million more daily things I'm thankful for: great weather, good running trails, Dr Who on instant Netflix, insane genes that allow me to eat my weight in sugar and not get diabetes, sunshine, laughter, and so much more. Even though it's taking me a few months to save the extra cash I'm finally going to be able to buy a sewing machine and I'm so excited to start sewing again. I want to try my hand at DIY clothes/up cycling and quilting. I'm hoping to be able to post more about cheap DIY projects.

Saturday, February 23, 2013

GOAL

I'm 90% I didn't do the last few days on my 14 days of Love blog thing. I was so out of it on cold medication last week I honestly don't care. I'm finally coming through the worst of it though. My sore throat has disappeared and now I'm just a walking bucket of snot. Which actually isn't too bad; at least I can blow my nose and move on with my life without having to take intense medication that makes me a walking zombie.

So I spent a couple of days doing my best to map out my financial future. It's imbedded in my DNA to try to plan and organize even if it's silly. My life sometimes feels like a series of jokes and downfalls of my plans. What is that saying? "Best laid plans"? I'm making this financial map with a big, giant, humongous grain of salt. I know things occur, I know bad stuff comes up, I know that there will always be road blocks to my goals. HOWEVER, I will work my hardest to reach my goal so I can finally be debt free.

Using an Excel spreadsheet I worked out the numbers if I continue to pay $1745.60 a month in student loans. My original deal with Wells Fargo was a $90,000 loan on a 30 year repayment plan that when calculated with interest will eventually cost me around $230,000 to pay back. BUT, if I stick to my twice a month payment planing (paying a total of $1745.60 a month) I will finish paying off my loan by April 1st of 2018.

It's both amazing and heartbreaking for me to potentially be free of this loan in 5 years. Amazing because not many people can rid themselves of such a large amount of debt in such a short amount of time. Heartbreaking because even though I'll finally be free of debt I'm going to have to miss out on so much. I'll be 33 the time this is (maybe) over. Only then will I be able to start saving for a house and that will take me a few years to do. By the time I can afford a house payment I'll be (probably) 35 or 36. Only then will it be responsible to have children (at least for me). I'm still partially on the fence about having children but I know that if I was to have them I'd want it to be earlier than that. I sometimes think it's best to put away certain life plans because it makes me feel too sad about my current situation. Luckily, I doubt I'll ever get married which (for me) is such a blessing because I could never afford a wedding (even one of those super adorable cheap-y Pinterest weddings).

I don't want this post to be a super bum out, even if I am feeling pretty bummed out right about now. For the past few years my heart has been pulled toward fostering children. Maybe this whole debt thing is to prevent me from having my own biological children because I have a bunch of lovely foster children just waiting for me. I would love to hit 33, be debt free, start creating my dream home and then bringing in loads and loads of children who just need love. I babysit for a friend of mine sometimes and baby's are hard. They crawl everywhere and it's your job to teach this little thing how to be a person. That's a pretty insane thing to do. When you foster children you get this lovely little human who pretty much already knows the basics and it's your job to love them and give them a better home than what they came from. How easy is that?!?! These children come from terrible homes with drug addicted and abusive parents. To be a great parent to them you just have to be there and be healthy and loving. I'm awesome at that.

I figured out a way to make this repayment a little easier to swallow. A reward system (a reward other than the joy I get from not being in debt). Every time I pay off $10,000 in principle I get to buy myself a present. With each $10,000 principle pay off the gifts can get better. They can be whatever I want. I've estimated paying off $10,000 in principle by September 2013 and I've already started thinking about what I want. Nice makeup? Some new clothes? Basically, I want to drop $50-$100 on myself. Yes, that money could go towards my loans but it's nice to treat yourself.

Tuesday, February 12, 2013

14 Days of Love

Yikes, time flies! I don't know how people manage blogs and full time jobs. And those mommy bloggers, how do they manage a houseful of kiddos and trying to make insightful, fun, and helpful blog posts?! So, time obviously slipped by but at least this time I have an excellent excuse. I'm totally coming down to with the sickies; months of allergies have finally taken their toll and I'm shacked up in bed with a major sore throat and hacking cough. But the blog must go on so here are Days 6 through 12 for my two week celebration of love :)

Day 6: Sweets Made Easy

I really love Bakerella and I REALLY love when she posts easy to make sweets. I've saved a few of the more advanced creations for further down. Here are a few of my favorite easy sweets from Bakerella:

Red Velvet Whoopie Pies: Love treats that are easy to eat and get festive with the red and white.

Cheesecake Pops: Easy and versatile, a recipe that can be adapted for any holiday.

Day 7: Not So Easy Sweets

Vintage Valentine Cookies: Not necessarily tricky for the recipe but I've always had major issues with printers. If you have access to a great one this is a must try recipe. So cute and a definite show stopper.

14 Layer Chocolate Cake: Absolutely messy and gorgeous, I bet this cake tastes divine. The time and care to create all 14 layers is definitely a labor of love.

Day 8: Dang Near Impossible Sweets

Rose Cupcakes: These cupcakes are almost too gorgeous to eat. I can barely draw a circle let alone craft fondant roses.

Box of Chocolates Cake: This is definitely in my top 5 of Bakerella creations. The little details on all of the individual cake pop chocolates are so adorable.

Day 9: DIY Gifts

Day 10: DIY Decorations

BrightNest has some amazing decoration ideas.

Day 11: Fancy Dinner

A great valentine's dinner doesn't have to cost an arm and a leg, Just pick a meal you both love, grab some of those lovely desserts from above and enjoy each others company by candlelight. Throw in some extra love by doing the dishes afterwards ;)

Day 12: Romantic Picnic

Same principle as a fancy dinner just outside. Go to a spot that's special to you as a couple (first kiss, first date, etc) and enjoy the scenery. A day spent soaking up the sun cuddled up next to someone you love is a beautiful thing.

Day 6: Sweets Made Easy

I really love Bakerella and I REALLY love when she posts easy to make sweets. I've saved a few of the more advanced creations for further down. Here are a few of my favorite easy sweets from Bakerella:

Red Velvet Whoopie Pies: Love treats that are easy to eat and get festive with the red and white.

Cheesecake Pops: Easy and versatile, a recipe that can be adapted for any holiday.

Day 7: Not So Easy Sweets

Vintage Valentine Cookies: Not necessarily tricky for the recipe but I've always had major issues with printers. If you have access to a great one this is a must try recipe. So cute and a definite show stopper.

14 Layer Chocolate Cake: Absolutely messy and gorgeous, I bet this cake tastes divine. The time and care to create all 14 layers is definitely a labor of love.

Day 8: Dang Near Impossible Sweets

Rose Cupcakes: These cupcakes are almost too gorgeous to eat. I can barely draw a circle let alone craft fondant roses.

Box of Chocolates Cake: This is definitely in my top 5 of Bakerella creations. The little details on all of the individual cake pop chocolates are so adorable.

Day 9: DIY Gifts

BrightNext has some great gift ideas (see below for great decoration ideas too!!)

Day 10: DIY Decorations

BrightNest has some amazing decoration ideas.

Day 11: Fancy Dinner

A great valentine's dinner doesn't have to cost an arm and a leg, Just pick a meal you both love, grab some of those lovely desserts from above and enjoy each others company by candlelight. Throw in some extra love by doing the dishes afterwards ;)

Day 12: Romantic Picnic

Same principle as a fancy dinner just outside. Go to a spot that's special to you as a couple (first kiss, first date, etc) and enjoy the scenery. A day spent soaking up the sun cuddled up next to someone you love is a beautiful thing.

Tuesday, February 5, 2013

14 Days of Love: Days 4 and 5

I'm doing a series on easy, fun, cheap ways to celebrate Valentine's Day. Click here to read about days 1 through 3. Today I'm covering days 4 and 5.

Day Four: Do something you hate

Now, take this with a grain of salt, I'm not recommending doing anything that makes you scared, uncomfortable or uneasy but an easy way to show someone that you care is to do something solely because it makes them happy. I enjoy a clean house, today is my day off and I've already put away laundry, done multiple loads of dishes, swept, vacuumed (you get my drift). My boyfriend is not a cleaner. Frankly, he's pretty sloppy. I will admit that there are times that it drives me crazy, there's nothing worse than feeling like your mate's personal maid. So, on the days that I come home and see that he's done the dishes, put away his clothes or done ANYTHING to clean up it makes my little black heart swell with love. My guy enjoys documentaries and art films while I enjoy action packed blockbusters so we make sure to go to both. Go on a hike, go to a museum just do something to celebrate your partners interests and likes.

Day Five: Make a mix tape (or a mix cd or play list for you hipsters)

I will never stop loving mix tapes. I know that technology is old and dated and frankly impractical but it is seriously the most romantic thing a fella can do (at least for me). Now I'm not saying that a mix cd has no love but it doesn't even take close to the amount of time and effort a good mix tape requires. Don't even get me started on an iPod playlist. That's just a few clicks you lazy bastards. Maybe I'm biased because the first guy I ever loved used to make me the most amazing mix tapes filled with artists I still love. I still have these tapes 10 years later (my love for them lasted a lot longer than my love for that guy). A Valentine's mix tape has to have a love theme or share some romantic significance for you and your partner. Here are a few of my favorite love songs (please don't judge my love for pop-punk):

Click Links for the youtube videos!

The Avett Brothers: Live and Die

Alkaline Trio: Clavicle

The Ataris: I Wont's Spend Another Night Alone

***you thought I was kidding about really enjoying music that was only vaguely good 10 years ago, jokes on you****

Blink 182: I'm Lost Without You

The Beach Boys: God Only Knows

The Honorary Title: Cut Short

A New Found Glory: Connected

A New Found Glory: Too Good To Be

The Lumineers: Stubborn Love

The Cure: Love Song

Court Yard Hounds: See You in the Spring

Plain White Ts: 1 2 3 4

Sam Cooke: Wonderful World (I think this is one of my favorite love songs ever, so classic)

Keane: Somewhere Only We Know

Yeah Yeah Yeahs: Maps

Also, I thought I had a ton of love songs for this list but after going through all my records, the internet, my ipod, etc I realize I just have a fairly long list of songs about how incredibly sad you can be after breakups. Seriously. I had to google love songs because apparently my music taste is 50% upbeat music to run to and 50% songs to listen to when you're on the edge of suicide after failed love. I should probably look into that because it doesn't seem healthy.

Day Four: Do something you hate

Now, take this with a grain of salt, I'm not recommending doing anything that makes you scared, uncomfortable or uneasy but an easy way to show someone that you care is to do something solely because it makes them happy. I enjoy a clean house, today is my day off and I've already put away laundry, done multiple loads of dishes, swept, vacuumed (you get my drift). My boyfriend is not a cleaner. Frankly, he's pretty sloppy. I will admit that there are times that it drives me crazy, there's nothing worse than feeling like your mate's personal maid. So, on the days that I come home and see that he's done the dishes, put away his clothes or done ANYTHING to clean up it makes my little black heart swell with love. My guy enjoys documentaries and art films while I enjoy action packed blockbusters so we make sure to go to both. Go on a hike, go to a museum just do something to celebrate your partners interests and likes.

Day Five: Make a mix tape (or a mix cd or play list for you hipsters)

I will never stop loving mix tapes. I know that technology is old and dated and frankly impractical but it is seriously the most romantic thing a fella can do (at least for me). Now I'm not saying that a mix cd has no love but it doesn't even take close to the amount of time and effort a good mix tape requires. Don't even get me started on an iPod playlist. That's just a few clicks you lazy bastards. Maybe I'm biased because the first guy I ever loved used to make me the most amazing mix tapes filled with artists I still love. I still have these tapes 10 years later (my love for them lasted a lot longer than my love for that guy). A Valentine's mix tape has to have a love theme or share some romantic significance for you and your partner. Here are a few of my favorite love songs (please don't judge my love for pop-punk):

Click Links for the youtube videos!

The Avett Brothers: Live and Die

Alkaline Trio: Clavicle

The Ataris: I Wont's Spend Another Night Alone

***you thought I was kidding about really enjoying music that was only vaguely good 10 years ago, jokes on you****

Blink 182: I'm Lost Without You

The Beach Boys: God Only Knows

The Honorary Title: Cut Short

A New Found Glory: Connected

A New Found Glory: Too Good To Be

The Lumineers: Stubborn Love

The Cure: Love Song

Court Yard Hounds: See You in the Spring

Plain White Ts: 1 2 3 4

Sam Cooke: Wonderful World (I think this is one of my favorite love songs ever, so classic)

Keane: Somewhere Only We Know

Yeah Yeah Yeahs: Maps

Also, I thought I had a ton of love songs for this list but after going through all my records, the internet, my ipod, etc I realize I just have a fairly long list of songs about how incredibly sad you can be after breakups. Seriously. I had to google love songs because apparently my music taste is 50% upbeat music to run to and 50% songs to listen to when you're on the edge of suicide after failed love. I should probably look into that because it doesn't seem healthy.

Subscribe to:

Posts (Atom)